Indian Pension System Introduction

- The Indian pension system has undergone three major phases: the Old Pension Scheme (OPS), the New Pension Scheme (NPS), and the proposed Unified Pension Scheme (UPS). Each phase represents a shift in policy, with varying impacts on retirees.

- The OPS was viewed as more secure, offering guaranteed benefits, while the NPS introduced market-linked investments, making retirement funds susceptible to market fluctuations. In response to a global shift away from neoliberalism, India has revisited its pension policies and introduced the Unified Pension Scheme (UPS) as a new approach.

Different Pension Schemes in India

- Old Pension Scheme (OPS):

-

-

- Coverage: Applicable to all government employees appointed before January 1, 2004.

- Defined Benefit Scheme: Provides a fixed pension of 50% of the last drawn salary plus Dearness Allowance (DA).

- Government Funded: The entire pension liability is borne by the government, with fixed returns guaranteed on contributions made to the General Provident Fund (GPF).

- No Employee Contribution: Unlike other schemes, the employee did not need to contribute towards the pension corpus.

-

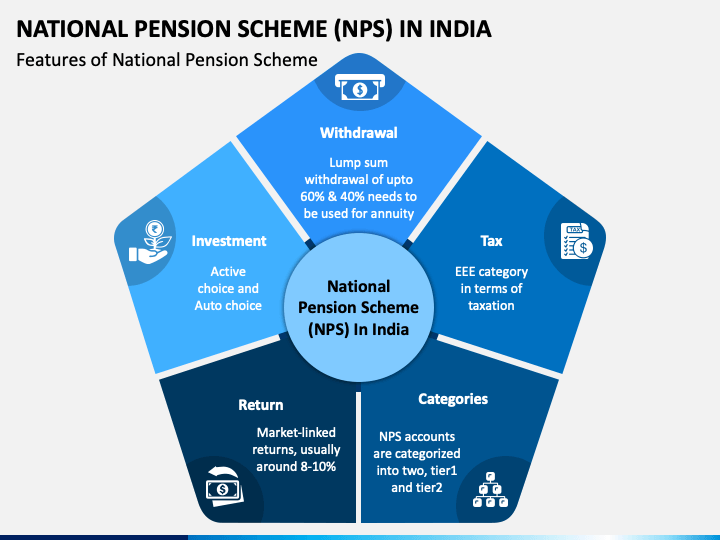

- National Pension System (NPS):

-

-

- Coverage: Introduced on January 1, 2004, for all central government employees joining after this date. State governments had the option to join, and all states except West Bengal and Tamil Nadu transitioned to NPS. Rajasthan, Chhattisgarh, Jharkhand, Punjab, and Himachal Pradesh have since shifted back to OPS.

- Defined Contribution Scheme: Employees contribute 10% of their basic pay and DA, with an equivalent contribution by the government.

- Market-Linked Returns: The pension benefit depends on factors like contribution amount, age at joining, type of investment, and investment returns. Unlike OPS, it does not provide a defined benefit.

- Voluntary for Unorganized Sector: The unorganized sector workforce can voluntarily enroll in NPS to avail of retirement benefits.

-

- Unified Pension Scheme (UPS):

-

- Coverage: Effective from April 1, 2025, for all those who retired under the NPS since 2004. It remains optional for employees to switch from NPS.

- Current Applicability: Initially applicable to central government employees; states can adopt it.

- Assured Pension: Offers a guaranteed pension, protecting against market uncertainties.

- Hybrid Features: Combines features of both OPS and NPS—provides assured pension like OPS and involves employee contributions to the pension corpus like NPS.

- Funded Scheme: Unlike OPS, which is unfunded, the UPS is contributory and funded, ensuring sustainable pension payouts.

Concerns with the Old Pension Scheme (OPS)

- Limited Coverage: OPS was limited to government employees, covering only about 12% of the total workforce in India. The introduction of NPS aimed to widen coverage to include the unorganized sector, where workers could join voluntarily.

- Fiscal Burden: The rising salaries due to Pay Commission revisions led to a surge in pension payouts under OPS, creating a heavy fiscal burden on both central and state governments.

-

-

- Example: The expenditure on civil service pensions was around 2.31% of GDP in 2004-05, and the implicit pension debt stood at approximately 56% of GDP, according to the India Pension Research Foundation.

- Intergenerational Liability: OPS relied on the current workforce’s contributions to fund pensions, leading to a transfer of resources from current taxpayers to retired employees. This created a significant financial burden for future generations.

-

- Early Retirement Disincentive: OPS provided a fixed pension of 50% of the last drawn salary, discouraging early retirement. Employees, even if disengaged, tended to continue until retirement age to avail the maximum pension, resulting in inefficient utilization of human resources.

Advantages of Introducing NPS

- Investment Choice: NPS allows subscribers to choose their fund manager and preferred investment options, such as a 100% government bond option. A guaranteed return option is also available for those seeking assured annuities.

- Example: Subscribers can choose between various fund managers like SBI Pension Funds, LIC Pension Fund, etc., based on their risk tolerance.

- Permanent Account: Subscribers receive a Permanent Retirement Account Number (PRAN), which remains valid for life, simplifying pension management.

- Job Portability: PRAN remains unchanged even when switching jobs, ensuring portability of the account across different employment types.

- Oversight Mechanisms: The NPS is managed by an NPS Trust that oversees the performance of fund managers. A trustee bank efficiently manages fund flows, and a custodian holds the securities.

Issues with the Introduction of NPS

- Exposure to Market Risks: Contributions under NPS are invested in the financial markets, making the returns dependent on market conditions. This causes uncertainty compared to the Old Pension Scheme.

- Example: According to an SBI report, NPS asset growth in 2022 was impacted by the Ukraine-Russia conflict, potentially falling short of the target of Rs 7.5 lakh crore by March 2022.

- Employee Contribution: Unlike OPS, where the government funded the pension entirely, NPS requires a monthly contribution of 10% of basic pay and DA from employees. This reduces the disposable income available to employees while they are still in service.

- Example: An employee earning a basic pay of Rs 50,000 and DA would need to contribute Rs 5,000 monthly, affecting their current cash flow.

- No Fixed Returns: The fixed returns guaranteed for GPF contributions in OPS are not available under NPS. The absence of GPF provisions in NPS means employees do not receive the guaranteed returns that were previously assured.

- Dependence on Market-Linked Corpus: Unlike OPS, where family pension was assured, the NPS pension benefits depend entirely on the accumulated corpus, which might vary with market conditions, thus lacking security for dependents.

- No Protection Against Inflation: The NPS does not provide inflation-indexed returns. As the pension amount is entirely market-linked, it does not automatically adjust with inflation, potentially eroding purchasing power over time.

- Example: An employee receiving a pension of Rs 20,000 under NPS may find its value diminished over years due to inflation, unlike OPS which adjusts the pension with inflation-linked Dearness Allowance.

Significance of the Unified Pension Scheme (UPS)

- Guaranteed Benefit: The UPS offers a fixed, assured pension amount, providing greater predictability than the market-linked NPS. Employees with a minimum of 25 years of service will receive a pension equivalent to 50% of their last drawn salary from the previous 12 months.

- Increased Financial Security: The government contributes 18.5% of an employee’s salary under UPS, which is higher than the 14% in NPS, significantly boosting the pension corpus and ensuring better financial security during retirement.

- Example: An employee with a basic salary of Rs 50,000 would receive an additional Rs 9,250 annually due to the increased government contribution, compared to the NPS.

- Protection Against Inflation: Employees with over 25 years of service are eligible for inflation-linked increments post-retirement, which ensures the real value of the pension remains intact despite rising living costs.

- Example: An employee receiving a pension of Rs 25,000 may get periodic increments to offset inflation, maintaining their purchasing power.

- Financial Support for Dependents: UPS ensures a family pension of 60% of the employee’s basic pay, which is paid to the dependents in the event of the employee’s death. This provides crucial financial security for the family members of the deceased employee.

- Combination of Defined Benefits and Contributions: UPS incorporates the stability of OPS’s guaranteed pension and the portability and investment flexibility of NPS, offering both security and growth potential for retirement benefits.

Concerns with the Unified Pension Scheme (UPS)

- Government’s Financial Liability: Providing a defined pension significantly increases the financial burden on the government.

- Example: In the first year of implementation, the government would need to spend Rs 800 crore on arrears, and the ongoing pension liabilities would cost around Rs 6,250 crore.

- Impact on Government Expenditure: The defined benefits under UPS may lead to unsustainable liabilities, potentially limiting government expenditure on other essential public services due to the larger budget allocated to pension payments.

- Limited Coverage: The scheme is primarily for central government employees, leaving out a vast majority of the workforce. Unlike NPS, which was also voluntary for unorganized sector workers, UPS has no provisions for them, leading to inequitable retirement benefits.

- Management of Existing Corpus: The transition from NPS to UPS raises challenges regarding the management of the accumulated NPS corpus and may discourage future participation in NPS due to uncertainties around the shift.

- Lower Investment Returns: Critics argue that the returns under UPS may be lower compared to the defined benefits under OPS, and retirees may face vulnerability to market risks. Additionally, concerns about underfunding could result in delayed pension payouts, negatively impacting retirees’ financial stability.

- Minimum Service Requirement: The requirement of 25 years of service to qualify for the full pension is disadvantageous for those who join government service late in their career, as they may not qualify for the full benefits.

- Exclusion of Public Sector Workers: UPS currently covers only central government employees and excludes many public sector workers, potentially hindering future pay commission decisions, creating inequities between different categories of public service employees.

Comparative Analysis of Pension Schemes

- Pension Amount:

- Old Pension Scheme (OPS): Provides a fixed pension equivalent to 50% of the employee’s last drawn salary, ensuring stable income after retirement.

- National Pension System (NPS): Offers a market-linked pension. There is no defined pension amount, and the actual pension depends on the performance of the chosen investment funds.

- Unified Pension System (UPS): Guarantees a pension of 50% of the average basic pay from the last 12 months prior to retirement, combining predictability with flexibility.

- Inflation Indexation:

- OPS: Pension is adjusted for inflation through the Dearness Allowance (DA), helping retirees maintain their purchasing power over time.

- NPS: No provision for inflation adjustment, making pension benefits susceptible to inflation, as the returns are market-dependent.

- UPS: Pension is indexed to inflation, based on the All India Consumer Price Index for Industrial Workers (AICPI-IW), ensuring stability in purchasing power.

- Employee Contribution:

- OPS: No employee contribution is required, as the entire pension is funded by the government.

- NPS: Employees contribute 10% of their basic pay and DA towards their pension. This helps build a retirement corpus, but it reduces disposable income during employment.

- UPS: Similar to NPS, employees contribute 10% of their basic pay and DA to ensure a contributory pension corpus while maintaining an assured pension benefit.

- Government Contribution:

- OPS: Fully funded by the government, meaning there is no contribution from employees, and the entire financial burden falls on the government.

- NPS: The government contributes 14% of the employee’s basic pay and DA, assisting in building the pension corpus without fully bearing the pension burden.

- UPS: The government contributes 18.5% of the employee’s basic pay and DA, higher than NPS, boosting the retirement corpus and providing greater financial security.

- Family Pension:

- OPS: Provides a family pension that continues after the retiree’s death, offering financial security to dependents.

- NPS: Family pension depends on the pension corpus accumulated by the employee. If the corpus is insufficient, it may result in lower financial support for dependents.

- UPS: Ensures an assured family pension, which is 60% of the employee’s pension, providing dependents with consistent support.

- Risk:

- OPS: No market risk involved, as the pension is fully assured and guaranteed by the government.

- NPS: Exposed to market risk as pension benefits depend on the returns from investments, making it potentially volatile.

- UPS: Faces lower market risk compared to NPS, as it guarantees an assured pension, combining elements of predictability from OPS and investment from NPS.

- Flexibility:

- OPS: Has low flexibility since benefits are fixed and predetermined by the government. Employees have no choice regarding their pension contributions or management.

- NPS: Highly flexible, allowing employees to choose fund managers and investment options. It offers multiple options like equity, corporate bonds, and government bonds.

- UPS: Offers limited flexibility with an assured pension structure. While it has a contributory element, it lacks the investment choices available in NPS.

Way Forward

- Broaden Coverage: The UPS should be expanded to include informal labor, which constitutes a significant portion of India’s workforce, thereby ensuring pension security for all citizens, not just government employees.

- Increase Government Contribution: To make this inclusion feasible, the government could increase its contribution rate, making the scheme attractive and viable for workers in the informal sector.

- Periodic Financial Assessments: Regular evaluations should be conducted to assess the financial sustainability of UPS. These assessments would help ensure that the government contributions are adequate while balancing fiscal responsibility.

- Gather Feedback: Ongoing consultations with stakeholders such as government employees, unions, and pensioners’ associations are essential to gather feedback and address concerns. This participatory approach can improve transparency and refine the scheme as per employee needs.

- Monitor and Evaluate: The government should establish clear performance metrics to evaluate the effectiveness of the UPS in meeting its objectives. Metrics like financial stability, satisfaction rates, and pension adequacy should be tracked to make informed adjustments.